Scenius Insights: On Blockchain Valuations

Special Guest Post from Decentral Park Capital Research

Scenius: The intelligence and the intuition of a whole cultural scene. The communal form of the concept of genius.

Welcome to Scenius Insights — a Scenius Capital publication platform for crypto and blockchain thought pieces, research, market commentary, and occasional musings.

This issue of Scenius Insights is prepared and contributed by Decentral Park Capital Research. Decentral Park is a founder-led cryptoasset investment firm comprised of team members who’ve honed their skills as technology entrepreneurs, operators, venture capitalists, researchers, and advisors.

If you would like to contribute your thought piece or research for publication to Scenius Insights, please reach out. And if you find this newsletter valuable, please subscribe and share Scenius Insights with your network 💪

On Blockchain Valuations

A refreshed exploration into valuation lenses for public blockchain networks

Lewis Harland, Portfolio Manager & Head of Research, Decentral Park Capital

Key Takeaways

Valuation methodologies for blockchain networks need to encompass both crypto-native inputs (on-chain economics) as well as pre-existing lenses (e.g. Metcalfe’s Law).

Current blockchain valuation models often don’t factor in shared value creation between systems (e.g. L1 <> L2) related to key factors like economics and active user bases.

The value of scaling networks can, at least in part, be driven by its contribution of economics (via gas fee markets) to its parent chain.

Metcalfe Law-type valuation models for Layer 1 blockchains perform better since the advent of scaling networks if they factor in the active user base contributing resources directly/indirectly to the L1 via scaling networks.

Lindy effects may mean longer-standing L1 blockchains are valued higher as a function of their active user base but the market becomes impartial during the late innings of a bull market.

There is some evidence that each additional user in a growing L1 or scaling network may be valued less over time although more data is needed.

As an industry, we are only just starting to articulate and understand the value captured by blockchains.

One under-researched area is gas markets where fees are paid by network users who want to transact.

For Ethereum today, fees are split into two: the base and miner tip fees. The base fees for every Ethereum transaction flow indirectly to token holders via burned transaction fees after EIP-1559 went live. $9.16B of fees alone have been burned since EIP-1559.

The additional miner tip goes to block producers directly after the network switched from Proof-of-Work to Proof-of-Stake.

Over 30% of total block producer fees are now comprised of transaction fees. Note, pre-merge, the revenue sourced from transactions amounted to just 6% although this was largely due to the removal of the miner subsidy.

Still, the month-on-month climb in this ratio indicates that transaction fees have become a much more significant source of economics for block producers (previously miners). One reason is that users are willing to pay more to use Ethereum.

Users are burning a total of 907k ETH/year with $9.16B total number of ETH burned since EIP-1559 and $1.86m over the past year. Factoring in block producer fees too and you get a $220B valuation that’s ~70x revenue.

Understanding crypto network valuations is to understand their crypto-native economics and their evolution.

Enter scalability networks.

Before the advent of scaling solutions, on-chain fees prohibited lower-value users from participating in the network. Networks like Polygon or Optimism that plug into the Ethereum base layer tackle this problem directly by offering a cheaper, more scalable solution for these lower-value users.

There will likely be multiple value settlement ‘lanes’ for different market participants. A high-net-worth individual may choose to settle on Ethereum L1 while retail may feel comfortable in using an alternative value settlement lane like Optimism wherever possible.

Valuation Lens 1: Gas Contributions To Parent Chain

Scalability blockchains have grown to become a $14B+ market but what has been driving this valuation?

One approach is to value these scalability networks with respect to their gas contribution to their parent chain. This is because several scalability networks (whether a PoS Commit Chain or optimistic rollup chain) still ultimately rely on a parent chain like Ethereum for the system to operate.

For Polygon PoS, the checkpoints containing the transactions are submitted on Ethereum. For Optimism, Ethereum is levied as the ultimate verification layer (e.g. submitting state root) as well as housing funds within smart contracts.

Therefore, several L2s and PoS Commit Chains could be valued as a function of their economic contribution (or block space demand) back to their parent chain. One loose analogy within the Web2 sphere is Marqeta which needs the Cash App to generate tokenized cards (pre-paid direct debits). For crypto networks, you could replace Marqeta with a crypto network like Optimism that needs its Cash App - Ethereum.

See the Fintech Blueprint for quality analysis on Marqeta.

Through this lens, we can value a scaling network as a function of total gas contribution back to its parent chain.

Starting with Polygon’s PoS chain, we can see the value placed by the market appears to track the chain’s economic contribution (in this example gas contribution dominance) quite well over time.

Note that starting in early 2021, the market was starting to value MATIC in relation to Polygon’s block space gas dominance for Ethereum. But why then? Curve, Aave, Decentraland, and Sushiswap launched in April and May 2021 and we began to see real utility within the Polygon ecosystem - aided by a growing active user base (more on this later) that collectively drove the network’s TVL to $10B.

Charting the same for Optimism yields a very different result. The launch of the OP token in May 2022 started tracking the chain’s (limited) economic contribution back to Ethereum in the 3 months afterward.

Over Q3-Q4 2022, Optimism’s fair value ticked higher while the bear market and peak fear drove prices to floor bottoms. The sharp drive higher in economic activity can be largely attributed to Optimism’s “learn-to-earn” incentive program, Quest, which ended in January 2023.

Despite this collapse, OP went on to print new highs with the ATH being in line with Optimism’s economic contribution high in the index just a few months previously. Fast forward to today and both measures are now diverging the most since inception and remain to be seen if/when they converge.

Valuation Lens 2: A Revisit of Metcalfe’s Law

An alternative (but complimentary) valuation framework is Metcalfe’s law where the value of the PoS or L2 network is proportional to the square number of nodes within that respective network (n2).

For some time, this lens has been applied liberally to crypto networks by researchers.

Over the past several years, Ethereum’s network value has been tracking Metcalfe’s Law Index Model track well until they begin to diverge in January 2021. One explanation could be the bull market placed a premium on ETH relative to its ML fair value. However, there may be more to unpack here.

Tweaks in this valuation model like the GMI Network Value Model (described here as Metcalfe’s Law x Transaction Volume Index or MLTV index) value networks as a function of active users x the dollar/units of transaction volume. This approach has merit as it seems reasonable that the value of a network has to factor in the value shared across those active nodes.

In other words, the model would apply a higher value to a network with 1m nodes transacting $1B volume over time t than a network with the same number of nodes transacting just $1m.

However, our MLTV index starts to go off kilter for Ethereum from mid-2021 onwards.

What the MLTV Index doesn’t do is incorporate the active user sets that may be contributing economic activity to Ethereum as a parent chain. For example, the growth of Optimism’s active user set may feed up to Ethereum’s network valuation with the latter being used as the former’s verification layer.

Blockchain valuation metrics have to evolve to factor in possible changes in the economic connections between the systems. The burgeoning scaling ecosystems made this necessary back in 2021.

Let’s double-click on the active user set.

Networks that don’t have associated scaling networks still seem to be priced closer to their active user base fair value (if anything slightly below).

But how should we think about networks like Ethereum that do have scaling networks plugged into them?

As we mentioned earlier, scaling solutions like Polygon started to provide actual utility for lower-value users in early 2021.

This accelerated further with the advent of rollup-centric networks like Arbitrum and Optimism in 2022 which helped drive the total value deposited in L2s past $7B in March 2022. A consequence of this growth was a large number of addresses that ported over from Ethereum to scaling networks.

We can create a revised Metcalfe’s Law model that incorporates the active user base of leading scaling networks (called Metcalfe’s Law or ML).

Ethereum’s network valuation appears to track the blended model from Q4 2021 onwards better than Ethereum’s ML. Note, ETH’s price decline in the summer of 2022 fell in line with where the blended model printed ‘fair value’.

The gap between the blended model and Ethereum’s valuation at the peak of the bull market suggests that, to some degree, investors may have placed too much of a premium on ETH relative to its ML fair value.

Analyzing the individual scaling network can also illustrate the close tie between a network’s network valuation and its active user set but divergences do occur.

Optimism’s OP token has been overextending above its ML fair value for the majority of the time since its inception.

One explanation could be Optimism’s OP token being driven by the L2 and liquid-staking derivative narrative momentum that dominated the January-February 2023 period. In other words, the investor narrative is overextended relative to underlying usage amid a tightening cycle by central banks.

The second is that, unlike Polygon, Optimism is still a relatively nascent network and needs more time for maturity.

A third is that Optimism, as an L2, is priced differently based on its architecture than a standalone PoS Commit Chain to Ethereum such as Polygon. This warrants further exploration.

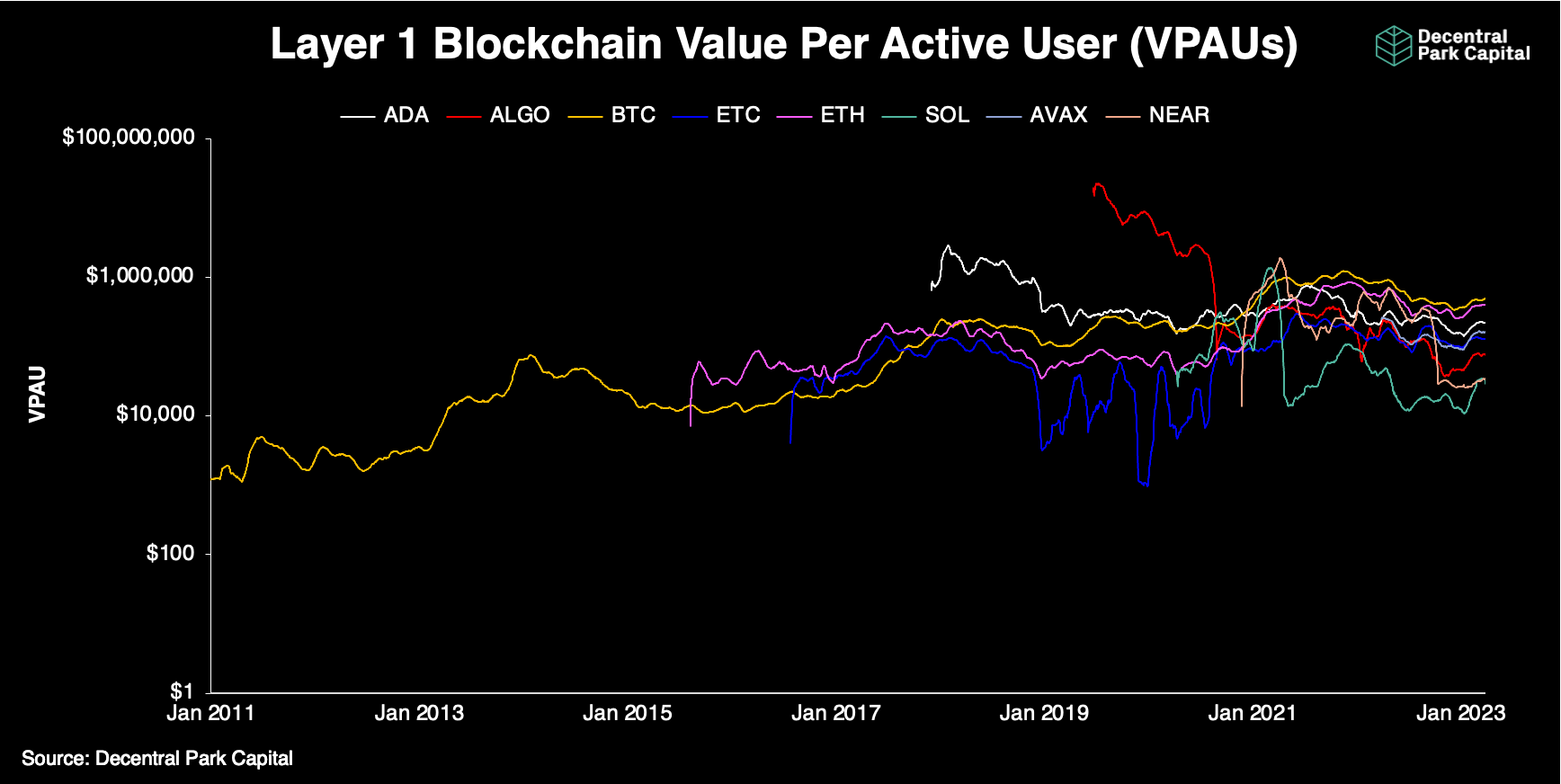

Valuation Lens 3: Value Per Active User (VPAs)

We can also analyze the market value placed on each user for a crypto network. Charting value per active user ratio (VPA) for several L1s shows:

1) Variation: longer-standing L1s appear to command a higher premium for each active user on that network (BTC, ETH).

2) Impartiality: early innings of bull market momentum can lead investors to initially value each active user the same (e.g. Dec-Jan 2021) only to then become more partial over time.

Today, Bitcoin and Ethereum have priced the same relative to their active user base and are the highest of the cohort. This suggests smart contract functionality is not a user input into Metcalfe’s Law-type valuation model.

Networks like Solana are priced relatively low as a function of their active user base. Longer-standing networks are commanding a premium.

Yet, could it be that the market is discounting these more nascent networks due to recent events? Possibly reflecting a recency bias? Is the flourishing of Ethereum’s L2 ecosystem diluting NEAR’s aim to offer a fully-sharded PoS chain for the mass adoption age?

The % gap between the maximum and minimum value also appears to increase over time with no ‘golden ratio’ being applied across the board.

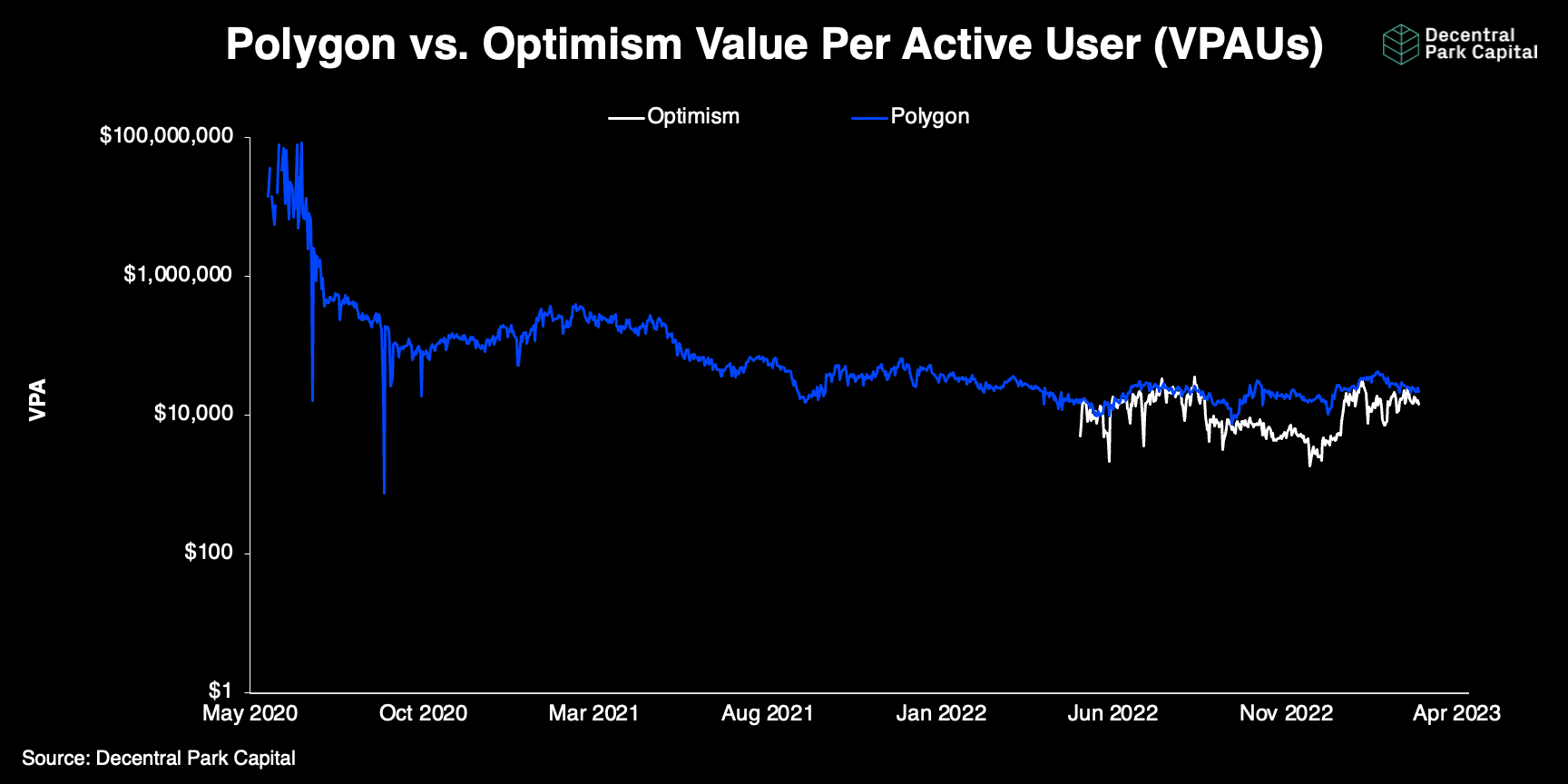

Scaling networks like Optimism and Polygon are priced generally the same now on a per active user basis ($20k/user) although we do see some variability.

Polygon’s general decline since inception hints that, as these networks mature and grow, a lower value is placed on each additional active network user in the total set. The first 1m users are more valuable when the network only has 2m users than when the network has 200m users.

These relative comparison analyses may also help us to understand mispricing in network valuations if divergences in these key metrics start to occur.

Final Thoughts

We are only just starting to understand how to identify and articulate key parts of the crypto value chain.

Understanding network valuation doesn’t require one measure but several: both crypto-native measures (e.g. gas economics, on-chain transaction volumes) and well as more generalized measures (e.g. Metcalfe’s Law).

Using several valuation methodologies may also be appropriate to construct a more comprehensive analysis. For example, OP’s value was in line with its ML value in Q 2022 - yet far below what the market was pricing the Polygon network relative to its active user base.

Over time, investors may also place a greater emphasis on certain measures over others as well as add new ones to the repertoire. The ever-evolving nature of crypto networks and the industry may drive an evolving set of valuation lenses which makes it all the more demanding but exciting to analyze.

Decentral Park Market Pulse

Want real-time updates and analysis on the digital asset market? Join Decentral Park’s Market Pulse group by clicking the link below:

Key Decentral Park Links:

> Decentral Park Research Hub

> Decentral Park Market Pulse

> Decentral Park Website

About Decentral Park

Decentral Park is a founder-led cryptoasset investment firm comprised of team members who’ve honed their skills as technology entrepreneurs, operators, venture capitalists, researchers, and advisors.

Decentral Park applies a principled digital asset investment strategy and partners with founders to enable their token-based decentralized networks to scale globally.

DISCLAIMER

The information above does not constitute an offer to sell digital assets or a solicitation of an offer to buy digital assets. None of the information here is a recommendation to invest in any securities.

Scenius Capital Management LLC, its affiliates or Funds are not providing any general advice or personal advice regarding any potential investment in any financial products. This letter is an informational document and does not constitute an investment recommendation. Information in this letter may include data and opinions derived from third-party sources. Scenius Capital Management LLC does not accept liability for the accuracy or completeness of any such information or opinions which can be subject to change without notice. The information set forth herein does not purport to be complete and no obligation to update or otherwise revise such information is being assumed.