Scenius Insights: Confluence

Special Guest Post from Motus Capital Management

Scenius: The intelligence and the intuition of a whole cultural scene. The communal form of the concept of genius.

Welcome to Scenius Insights — a Scenius Capital publication platform for crypto and blockchain thought pieces, research, market commentary, and occasional musings.

This issue of Scenius Insights is prepared and contributed by Motus Capital Management. Motus is a team of early crypto investors with extensive traditional finance experience in trading and asset management, applying fundamental research and disciplined portfolio construction to small- and mid-cap liquid tokens.

If you would like to contribute your thought piece or research for publication to Scenius Insights, please reach out. And if you find this newsletter valuable, please subscribe and share Scenius Insights with your network 💪

Crypto markets have seen great progress in 2024 in terms of user adoption, institutional acceptance, and increasing regulatory clarity, yet prices have chopped lower for the past 5 months. In Motus’ below missive, they explore the confluence of factors that explains this disconnect and what comes next.

Summary

The confluence of crypto institutionalization, rising global liquidity, removal of BTC supply overhangs, and election clarity provides an attractive setup for year end and beyond.

Intro

In August 2023 we authored the “The Start of the Next Cycle”, highlighting the number of factors coming together that would kickstart the next rally in crypto markets. From September 2023 through March 2024, Bitcoin rallied 175% (making a new all-time-high), and alternatives or “altcoins” like Solana rallied 915%, with significant dispersion amongst the rest.

The basis of that piece was the concept of crypto’s four-year price cycles, and the significant improvements in the underlying technology that would drive broader adoption, specifically: 1) improved scalability, 2) increased capital efficiency, 3) increased composability, and 4) better user experience to bring the next billion users onchain.

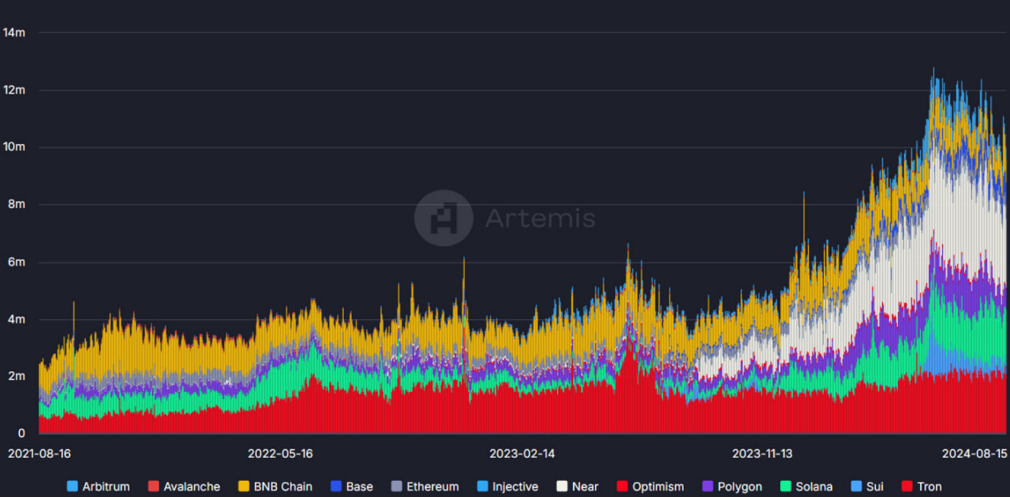

We believe these all hold true and are observable through a steady increase in daily users, volumes, and revenues generated by the crypto ecosystem.

Active Users

However, from April 2024 through August 2024 price momentum has been derailed, resulting in a peak-to-trough drawdown of ~30% for Bitcoin since the March $74,000 high to the August low to date of $49,000, with almost every other crypto asset faring worse. Some of which can be attributed to seasonally thin orderbooks, with most damage done due to a drop in US liquidity and the arrival of supply overhangs. Nonetheless, the top crypto assets by market cap have still outperformed equity markets year to date.

So what has happened and where do we go from here? With most supply overhangs in the rear-view, increased institutional ownership, improved macro conditions, and underappreciated fundamentals, we see a similar confluence occurring that should benefit the crypto market in an outsized way over the next 6 months and throughout 2025.

Supply Overhangs Removed, Demand Tailwinds to Come

2022 was one of the worst years on record for the crypto market. However, perhaps one of the only “winning” strategies was to buy announced bankruptcy dips, and there were several. The last of which was FTX in November 2022, dropping the price of Bitcoin to under $16,000, which marked the bottom of the bear market. The thesis was simple – once a company announces bankruptcy, they (and their customers) cannot sell their assets.

Over the past few months, we have seen the opposite effect – from companies finalizing bankruptcy proceedings and distributing crypto in-kind to German and US Governments distributing or selling Bitcoin they had seized in years past. This included $9B from the Mt. Gox seizure, and $2B from the Silk Road seizure, both over a decade ago. Supply overhangs since April in a seasonally low-liquidity market are outlined here:

• German Government: ~50,000 BTC between June 19 and July 13

• Genesis Bankruptcy: 33,000 BTC distributed to creditors in early August

• Mt. Gox Bankruptcy: 110,000 BTC distributed to creditors in July

• US Government: ~14,000 BTC transferred to Coinbase, presumably for sale

• Miners: post April’s quadrennial halving of BTC inflation, unprofitable miners sold BTC to shore up balance sheets or shut down

Fun fact: the US government has sold 195,000 BTC over the years for around $366MM. In August, they sold just 10,000 BTC for $600MM. Maybe those calling for a US Strategic BTC Reserve are onto something.

All told, $15+ billion in crypto has been sold or distributed from these entities since April this year. In our opinion, given developed futures markets and enormous global trading liquidity, this should have been absorbed, particularly given that in-kind distributions were highly unlikely to be sold in their entirety.

However, the opposite was true. For example, in June, the German government—who had already conveyed that they would be selling their 50,000 BTC — moved 2,000 BTC to an exchange. In a mature market, it would be obvious that selling 2K BTC, or even 50K BTC, should be a blip on the chart. BTC trades tens of billions of dollars per day, and this represents a fraction of a percent of supply. Instead, ~140K in paper BTC evaporated in response, and fears of selling overhangs overwhelmed the enormous success of BTC ETFs, which alone soaked up more than 100% of the German sales. This is much more consistent with a peer-versus-peer speculative asset than a mature, fundamental asset.

The point of all this is to say that supply side overhangs are mostly behind us, and that most crypto-native capital remains sidelined. Ironically, the FTX bankruptcy may provide another attractive entry point for investors.

For all of Sam Bankman Fried’s obvious faults and flaws, it turns out that time has proven him to be an astute investor. Due to the success of Anthropic and the FTX estate’s large SOL holdings, FTX creditors are expected to receive a full recovery on claims, paid out in cash.

In May, the FTX estate said it expects to have between $14.5 and $16.3 billion in cash available to distribute to creditors. Once the court approves the distribution plan, creditors will receive their cash within 60 days.

We anticipate distributions to occur in December or January, and it is likely that a portion of this cash is reinvested into crypto markets. Like the announced sales, we would expect this inflow to be front run, creating a multiplier effect on the dollar amount distributed.

Global Liquidity on the Rise

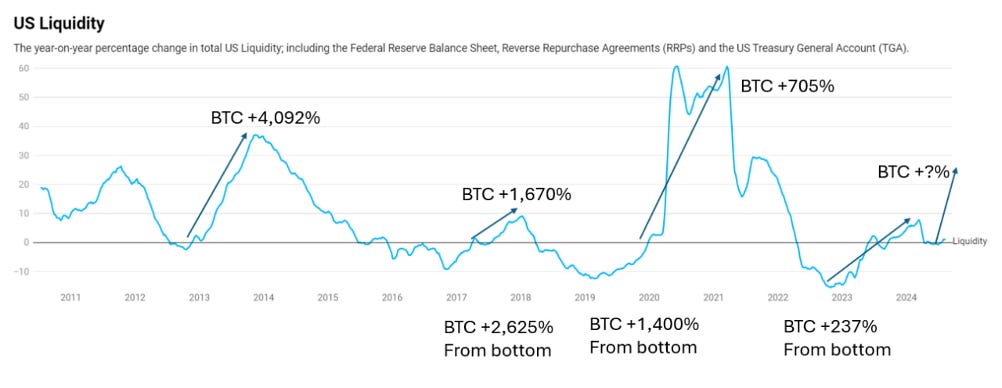

Bitcoin price is highly correlated to global liquidity. Global liquidity has bottomed and is starting to increase.

As referenced above, we’ve written about crypto cycles before, and they’ve remained reliable, but we haven’t discussed why they’ve played out how they have, and whether the factors driving those cycles will persist. Since financial assets are priced in US Dollars, it follows logically that the quantity of dollars and debt globally are a driver of asset prices. This isn’t the only variable, but in an emerging asset class without a long-term track record of valuation metrics to study, liquidity has an outsized impact. As central banks create more currency, assets with known capped supplies garner more attention.

It’s often said we won’t see another cycle like the one that was brought on by COVID-era stimulus, but liquidity is misunderstood—it’s cyclical over time, as central banks and treasuries respond to both the economy and their own desire to manage their balance sheets.

Liquidity is also not just rate cuts (although China and the ECB have commenced cutting, and the US Fed is about to get underway). It’s helpful to understand the other ways liquidity/dollars/debt enter the system and why. Currently, there are 3 other pools of money the Fed and Treasury can use to inject liquidity (which they are incentivized to do to boost assets and growth, and to increase their own tax receipts)—the Reverse Repo Program (RRP), the Fed overnight window for bank reserves, and the Treasury General Account (TGA).

The Reverse Repo Program sucks money out of money market funds when it pays more than short term debt instruments, and the Fed window sucks money out of banks that would otherwise be lent. Neither of these programs consist of assets that can be rehypothecated or levered or used for other assets, and instead they pull money out of the system that would otherwise invest in debt.

The unwind of this occurs when the Treasury wants to coax these dollars back off the Fed’s balance sheet back into the financial system to support increased treasury issuance (via slightly higher short term treasury rates vs. repo or Fed window rates). We have every reason to believe that in an election year, and with swelling debt and a challenging labor market, and when policymakers have a stated agenda to ease, they will use these tools.

Actually, they probably need to—the backdrop is $2T in planned deficit spending coupled with a global turning away from USTs, as China stockpiles gold and the JPY carry trade unwinds. The US Government needs to manufacture this demand for treasuries, and that means more debt/dollars in the system. Bank reserves constitute ~$3.3T, the TGA holds $750B, and the RRP represents ~$400 billion in potential liquidity additions. Some $300B from the RRP and TGA are already planned to unwind this year alone, and consider the move in BTC historically as the RRP was diminished:

The big picture is liquidity has cyclically bottomed, we are entering an easing cycle, and instead of COVID stimulus injecting liquidity, other policy tools will. This aligns with both incentives and stated policy. It has driven past crypto cycles, and prices will respond this cycle as they always have. This is best illustrated by the longer-term reaction of BTC to liquidity cycles:

Bitcoin’s Institutionalization

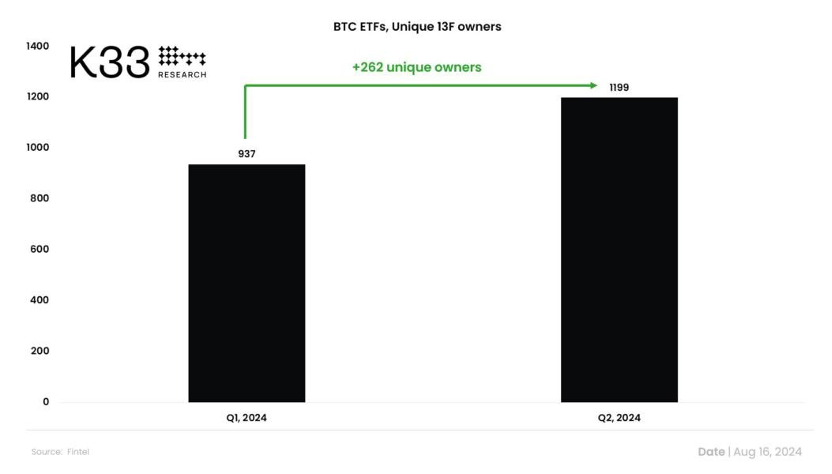

As of Q2 13F filings, 1,199 institutions filed ownership BTC ETFs, or 28% more than Q1. Blackrock’s IBIT has been the most successful ETF launch in history, and total ETF holdings are around $54B.

This seems fantastic, but in context, it just scratches the surface. Only a single-digit percentage of institutions have disclosed crypto ownership, meanwhile 75% of institutional participants planned to.

For all its success, Blackrock holds just 1.6% of BTC supply, while institutions hold ~80% of global equities. Further, in a recent survey of 130 Family Offices controlling roughly $60B in assets, 88% planned on increasing exposure to crypto this year, with only 2% planning on decreasing exposure.

The first wave of institutional adoption has seen small nimble players move first. Pension fund adoption includes Michigan and Jersey City, NJ pensions, but not Calpers. Sovereign level adoption includes El Salvador, but not the US. Small publicly traded companies have added crypto to their treasuries, but not the Magnificent 7 (other than Tesla). This is significant because the precedent is set, and the access points are established, but the biggest investors are yet to arrive.

While it’s difficult to say exactly who owns what onchain, with now over $100B of crypto in ETFs 8 months after their launch, it seems obvious that there is tremendous appetite, and yet ETFs are barely starting to get penetration compared to other asset classes, survey data, and the breadth of large participants who will soon join.

Beyond Bitcoin

We have made the case that the institutionalization of crypto has just started, Bitcoin ETFs are just ramping up, and that Bitcoin does well when global liquidity increases. What about the rest of the market?

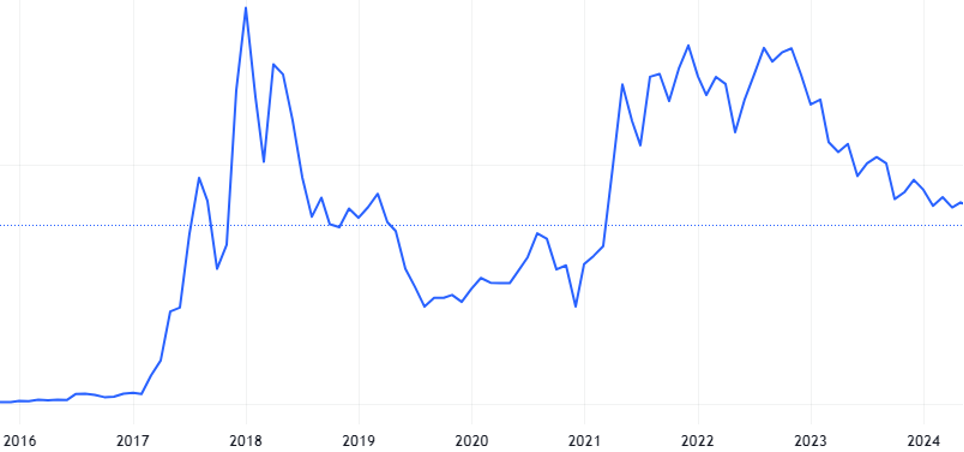

There have been two significant cycles in crypto that included assets outside of Bitcoin, with outsized gains witnessed in 2016 – 2017, and 2020 – 2021 (ETH launched in 2015). As you can see from the charts above this coincided with increases in global liquidity. We believe we are in the middle of the third cycle.

During the last two cycles, while Bitcoin produced significant returns ($1K to $20K in 2017, $8K to $69K in 2020-2021), the rest of the market grew multiples of Bitcoin. In the below chart we show the rest of the crypto market vs. Bitcoin during these cycles:

Crypto ex-BTC Mkt Cap / Bitcoin Mkt Cap – Source: TradingView)

Importantly, there was meaningful dispersion amongst assets outside of Bitcoin, with a handful of assets driving the outperformance. For example, in 2021 Bitcoin returned a modest 60%. Tokens that grew into the top 10 by market capitalization that year outperformed BTC by over 4,000% on average. The outperformance was even greater in 2017.

Of course, the assets that become cycle winners are not known in advance. Consider these stats:

• Only 2 of the top 10 tokens from 2017 are still in the top 10

• 60% of the top 10 tokens from 2020 lost top 10 status in 2021

• Multiple top performers in 2021 did not exist in 2020

• There has been 30% turnover in the top 10 so far in 2024

Dispersion and turnover of this magnitude offer incredible opportunities but requires an active approach.

Since 2021, only a few assets have reclaimed highs relative to BTC. We expect that to change as we close out 2024 and move into 2025. Of particular interest to us are protocols that generate significant revenue relative to market cap, and either a) currently return that to token holders via dividends or buybacks, or b) are expected to do so in the future. On its surface, this is an obvious area of opportunity. The reality is that most of these assets erased their year-to-date gains over the summer months, with some now negative since the start of the year.

There are a few reasons for this relative performance. For starters, intra-market correlation amongst crypto assets remains high, with most assets exhibiting high beta to Bitcoin directly associated with their market cap and associated liquidity profiles. Additionally, crypto markets are still relatively immature, and currently dominated by either participants without traditional market experience or traders attracted to high volatility. This creates distortions amongst highly speculative and non-revenue generating assets (ie. memes, AI tokens) and those that have actual revenue generating business models. In many ways, when the market goes risk-off, the proverbial baby gets thrown out with the bath water.

Where that leaves us are valuations that are too cheap to ignore. Consider the following “large cap” protocols:

In many cases, these protocols are making new all-time highs in fees monthly. However, price has not responded as one would expect. Going further down in market cap produces an even greater disparity between price return and fundamentals on specific assets.

We believe that the continued institutionalization of this market will lead to a greater focus on fundamentals. It is hard to envision a traditional fund or family office flocking to memes or high valuation decentralized AI plays that lack a finished product or users.

The key is understanding that not all revenues are created equal, and there is no standardized reporting (i.e. GAAP earnings) to rely upon. How these revenues accrue to holders differ asset-by-asset and are subject to change. Monitoring these changes often create the best buy or sell opportunities, and there are several examples to illustrate that this trend has already started:

AAVE – On July 25, 2024 a proposal was submitted to begin returning a portion of fees to AAVE token holders in the form of buybacks. Since then, AAVE has returned over 30% in dollar terms, outperforming the total market meaningfully over that time (shown below).

AAVE/TOTAL CRYPTO - TradingView

MKR – In June 2023, MakerDAO proposed a buyback mechanism using excess reserves. Over the next four months, MKR returned ~140%, again significantly outperforming the broader market.

MKR/TOTAL CRYPTO - TradingView

UNI – Uniswap has been the highest fee-generating protocol since its launch in 2018, but those fees do not currently accrue to UNI token holders. However, the concept of a “fee switch” has been discussed for years.

On February 23, 2024 a proposal was made to start returning a percentage of fees to UNI token holders. Within an hour, the UNI token appreciated over 40%. Unfortunately, this proposal was eventually removed, leading to a retracement in UNI price. It is highly likely we would see a similar reaction (directionally) if/when a new proposal is made.

There is a whole list of tokens that we believe are undervalued based on current fundamentals or will skyrocket if they turn on fee accrual to tokenholders.

Political Impact

The US election season is heating up, and there’s no shortage of speculation about what each candidate might mean for our industry. We’ll avoid that speculation for now and instead offer a few lesser-discussed perspectives.

First, BTC made new all-time highs under both former President Trump and current President Biden, despite both administrations previously taking a hostile approach to the new asset class.

Second, this is not a US-dependent asset class—it is digitally native therefore globally accessible. US support or a US BTC strategic stockpile would meaningfully accelerate adoption, but so far that certainly hasn’t been a requirement for success.

Third, while the US remains the financial and tech center of the world, only 7% of crypto businesses currently domicile here. Regulation matters, and of course we want a friendly administration, but hostility has mostly been impactful to timelines and the domicile of progress rather than progress itself.

Finally, while the executive branch and its appointees retain significant power to shape policy, the voices of citizens are increasingly being heard via Congress as well. FIT21 and the SAB 121 repeal both enjoyed bipartisan support, and pro-crypto PAC Fairshake continues to have an impressive record of shaping elections consequential to the industry.

Assuming the election remains Trump vs. Harris, investors should consider possible outcomes of each administration, and we’re ready to react either way.

Conclusion

An onslaught of supply from bankruptcies and government-seized Bitcoin from a decade ago put a lid on the Q1 rally. With large supply fears mostly behind us, continued institutional players entering the market for the first time, global liquidity on the rise, onchain fee-generating tokens with impressive growth at depressed valuations, and potential political clarity in the US, the setup is as, if not more attractive now as it was at “The Start of the Next Cycle” that began in late 2023.

About Motus Capital Management

Motus is a team of early crypto investors with extensive traditional finance experience in trading and asset management, applying fundamental research and disciplined portfolio construction to small- and mid-cap liquid tokens.

To learn more, visit their website at: www.motuscm.com