Protocol Highlight - GMX

GMX is a non-custodial, decentralized exchange (DEX) for spot and perpetual contracts that supports low-swap fees and zero-price impact trades, allowing users to leverage up to 30x.

2022 witnessed a series of failures by centralized entities in the digital assets sector as crypto lenders, exchanges, and funds imploded. Decentralized Finance (DeFi) has not experienced these same failings. Innovation continues and highlights the importance of blockchain alternatives that are permissionless, decentralized, and “on chain.” We believe continued scrutiny and pressures on centralized exchanges and entities will benefit decentralized alternatives. We take this opportunity to highlight one such protocol, GMX, whose token rose 15% in November, and doubled in 2022, as users flocked away from centralized options (such as FTX).

What is GMX?

GMX is a non-custodial, decentralized exchange (DEX) for spot and perpetual contracts that supports low-swap fees and zero-price impact trades, allowing users to leverage up to 30x. Non-custodial means that, unlike a centralized exchange, the protocol never takes custody of the users’ funds. Users simply connect their crypto wallets and can then deposit collateral directly into the platform’s smart contract where they have transparency into how the protocol works and can see transactions on a blockchain. Perpetual contracts refers to futures contracts that do not expire, instead remaining effective until the trader closes the position. Because perpetual contracts require relatively little collateral to support highly leveraged position, they are often used to speculate on crypto price action. Although risky, leverage trading is an essential part of the crypto ecosystem, allowing savvy participants to take advantage of drawdowns, manage risk, and make outsized bets.

GMX initially launched as Gambit Financial on the Binance smart chain (BSC), but later rebranded to GMX when it launched on Arbitrum, a layer 2 smart-contract scaling solution on Ethereum, in September 2021. It then launched on Avalanche, a high-speed layer 1 smart-contract blockchain, in early 2022. GMX is chain agnostic and has plans to expand to other chains in the future. Although anonymous, the founding team is known in the space and has built other respected products.

How does GMX work?

GMX uses an automated market maker model (AMM) that creates liquidity for both sides of trades and incentivizes liquidity providers. Liquidity providers deposit funds into GMX and receive trading fees from traders (supply-side fees). The protocol offers spot trading for a number of tokens and its perpetual swap markets allow traders to long or short major tokens with up to 30x leverage. This is not done through an order book, rather it is done through GLP, a shared liquidity mechanism that functions as a pool of all tradeable assets and takes the other side of all trades on the protocol so long as the GLP pool has available inventory. Trading is supported by this unique multi-asset pool that earns liquidity provider fees from market making, swap fees, leverage trading (spreads, funding fees & liquidations) and asset rebalancing. GMX lists only “blue-chip” tokens with substantial trading volumes and liquidity. This includes BTC, ETH, UNI and LINK. Traders can use any tokens that are included in the GLP pool for collateral. If the collateral token is different from the position token, GMX converts the collateral to the position token. When users exit a trade, they are able to exit via any of the GLP’s tokens.

Trades are made through prices provided via a Chainlink secured oracle that aggregates price feeds from leading exchanges and reduces liquidation risks from temporary wicks. Liquidations occur automatically when a user’s collateral becomes insufficient to maintain a trade and the platform forcefully closes the position and pockets the deposited collateral. Users must allocate separate collateral for different asset positions and there is no funding rate payments between long and short traders. However, traders benefit from the zero-price impact (no slippage), which is a positive differentiator for the platform. Traders pay trading and borrowing fees, which are split between GMX stakers and GLP token holders (ie: liquidity providers). GMX offers market, limit, and trigger order functionality, thus providing a friendly trading experience.

Source DeFi Llama

GMX rose to prominence in 2022 and became a significant player in the DEX space. As evidenced in the above chart, GMX managed to grow its TVL (Total Value Locked) and overall market cap through much of this recent bear market and into 2023, illustrating growing adoption and interest in the decentralized derivatives space.

The GMX & GLP Tokens

The GMX protocol has strong value accrual to GMX token holders and liquidity providers as the fees generated by the exchange are distributed entirely back to GMX and GLP holders. Holders receive rewards in the native blockchain token, meaning platform fees are paid in ETH on Arbitrum and in AVAX on Avalanche. GMX is the utility and governance token of the platform. The total supply of GMX is 13.25 million coins of which roughly 8.4 million (~63%) are circulating. GMX had what is commonly referred to as a “fair launch” meaning there were no venture capital or private sales to kickstart the project and all holders acquired their tokens via the open market. GMX holders can vote on proposals that shape the exchange’s future direction. It also allows stakers to receive 30% of the fees collected across the platform, escrowed tokens, and multiplier points to reward long-time holders.

GLP Token is the GMX Protocol’s native liquidity provider (LP) token and acts like an index of the large-cap assets supported by GMX, which exist within the multi-asset pool system. The token composition of GLP is slightly different on Arbitrum and Avalanche, and consists of a token and stablecoin mix that rebalances. The more optimized it is to meet the demand, the higher the utilization rate and fees returned to LPs; therefore, LPs are incentivized to contribute the tokens GLP needs via fee discounts. GLP can be minted using any of its index assets and burnt to redeem any index asset. It is automatically staked and non-transferable. GLP holders receive 70% of fees from the chain on which they reside. Because the GLP pool is the counterparty to traders on the exchange, if leverage traders win, GLP holders lose and vice versa.

The Competitive Landscape

DeFi alternatives for derivatives trading is a quickly growing sector of crypto. GMX is competing mainly in the decentralized perpetual futures market, but also competes as a spot market. GMX faces competition from more established as well as up-and-coming protocols, but the main vertical it appears focused on growing is the perpetuals market.

Source: tokenterminal.com as of February 2, 2023

GMX Prospects

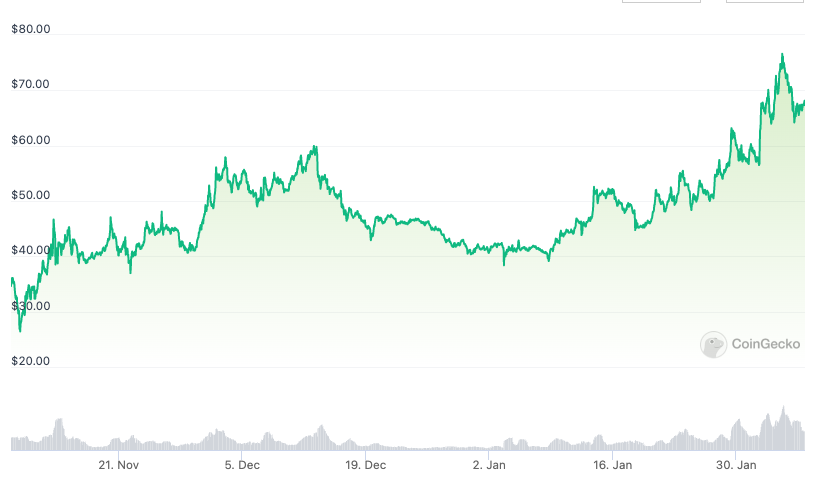

As evidenced in the above table, GMX has the highest circulating market cap after Synthetix (SNX), highest total value locked, almost 2,000 daily active users, and is generating nearly $13M in fees in a 30-day period. In 2022, the trading volume of the top 10 DEXes reached $1.33T with GMX gaining significant market share. According to TokenInsight’s 2022 Annual Report on Crypto Exchanges, GMX’s trading volume increased from 13.79bn in Q1 to 19.19bn in Q4, resulting in a remarkable increase of its market share of DEX trading volumes from 1.2% to 29.6%. The price of GMX also doubled in 2022 and has continued its positive momentum hitting a recent all time high of $70.65 on February 2, 2023 up 456% from its low of $11.53 on June 15, 2022.

Price chart of GMX in USD. Source: Coingecko

Conclusion

GMX is an interesting and viable alternative to centralized exchanges. It supports both spot swaps and leveraged trading of perpetual swaps and is a desirable trading venue given its zero-price impact design. GMX does not require KYC and is multi-chain with a plan to expand to other chains in the future. GMX should be well positioned to benefit from a continued shift away from calendar expiring futures towards perpetual swap markets, as well as a transition away from centralized exchanges to decentralized exchanges in light of recent events and anticipated regulatory scrutiny.

Reference Sources

1.https://gmx.io/#/

2.https://tokenterminal.com/terminal/projects/gmx

3.https://zerion.io/blog/what-is-gmx/

4.https://academy.binance.com/en/articles/what-is-gmx

5.https://medium.com/coinmonks/gmx-a-brief-explanation-a1f6ade01b04

6.https://defillama.com/protocol/gmx?hideEvents=true&showMcapChart=tru

7.https://www.gmxstats.com/

8.https://gmxio.gitbook.io/gmx/glp

9.Arun, Vikram, GMX: The Trading Platform of the People, by the People, for the People

10.Riley Substack, GMX Research Report

11.Perpetual Protocol Blog, What’s a Perpetual Contract?

12.https://www.coindesk.com/learn/what-is-a-perpetual-swap-contract/

13.https://insights.glassnode.com/the-week-onchain-week-17-2022/

14.https://cointelegraph.com/press-releases/four-years-of-deep-cultivation-mexc-perpetual-futures-liquidity-ranks-no-1

15.https://tokeninsight.com/en/research/reports/crypto-exchanges-2022-annual-report